nvestors sold U.S. dollars ahead of Friday’s nonfarm payrolls report and even the passing of the Health Care bill in the house failed to help the USD. Job growth is expected to be strong after last month’s big disappointment, particularly after the FOMC statement’s positive labor-market assessment. If you recall, economists in April were looking for payrolls to rise by 180K and the numbers came in at 98K, almost half that amount. So a rebound is expected Friday and an upward revision is even possible, especially given the Fed’s confidence in jobs and the optimistic views of fixed-income traders who continued to drive yields higher, keeping the odds of a June hike at a whopping 93.8%. However, having been burned 4 out of the last 6 months by missed nonfarm payrolls expectations, investors are looking at recent U.S. data and finding reasons to take profit on long dollar positions, especially in USD/JPY.

This month’s nonfarm payrolls report takes on exceptional importance because it will confirm or reject the market’s lofty expectations for a June tightening. The Federal Reserve won’t be able to raise interest rates if the labor data disappoints. And if there’s nothing positive in the report to offset the miss, the dollar will sell-off quickly and aggressively. However if job growth is as strong as the market anticipates (current forecast is 190k) and wage growth accelerates, USD/JPY will make another run to 113 and pairs like EUR/USD and GBP/USD will sink quickly. Taking a look at a number of related U.S. economic reports, there’s certainly reason for investors to be worried that Friday’s report may not live up to expectations. While jobless claims were very low and Challenger reported a steep decline in layoffs, the employment component of the manufacturing– and service-sector ISM reports continued to fall. Both reports accurately telegraphed the pullback last month and the fact that they did not improve is worrisome.

Arguments in Favor of Weaker Payrolls

- Employment Component of Non-Manufacturing ISM Falls Slightly

- Employment Component of Manufacturing ISM Falls Sharply

- ADP Drops to 177K from 255K

- Consumer Confidence Drops to 120.3 from 124.9

Arguments in Favor of Stronger Payrolls

- Continuing Claims Fall Below 2M

- 4-Week Average Jobless Claims Hover Near 40-Year Lows

- Challenger Reports Whopping -42.9% Drop in Layoffs

- University of Michigan Consumer Sentiment Index Rises Marginally

Meanwhile, Thursday’s best-performing currency was the euro, which rose to its strongest level in 5 months on the back of U.S. dollar weakness, healthier Eurozone retail sales and Emmanuel Macron’s solid performance at Wednesday night’s presidential debate in France. The latest polls show 61% in support for Macron and 39% for Le Pen, but with the U.S. election and Brexit still fresh on everyone’s mind, we could see profit taking on long EUR/USD positions before the London close Friday in the case of an upset. With that in mind, EUR/USD appears poised to test 1.10 in the coming days. Eurozone retail PMI numbers are scheduled for release Friday but the focus will be on NFPs. Sterling also extended its gains thanks to hotter service-sector activity. The PMI index rose to 55.8 from 55, driving the composite index up to 56.2 from 54.8. This completes the “trifecta,” with every part of the U.K. economy improving in April.

The commodity currencies were hit hard with USD/CAD rising to fresh 15-month highs. It’s been 10 trading days since USD/CAD has seen a pullback with the currency pair rising in 12 of the last 13 days. While its tempting to call a top, until oil prices bottom you can’t expect USD/CAD to stop rallying. Oil prices collapsed on Thursday, falling close to 5% to $45 a barrel. This is a potential point of support but oil can be very trending so it’s important to see prices stabilize before picking a bottom in crude and USD/CAD. At a minimum, USD/CAD could reach its next level of resistance at 1.38. A lot of which hinges on Friday’s U.S. and Canadian economic reports – Canada has employment and IVEY PMI numbers scheduled for release. The Australian dollar fell to a 3-month low while the New Zealand dollar sank to an 11-month low. Softer Australian data contributed to the move in AUD but the real catalyst was falling gold, iron ore and copper prices. Australia’s trade surplus shrank slightly in March while new home sales fell. Interestingly enough, the New Zealand dollar experienced steeper losses than AUD even though data remains steady with job ads continuing to rise, extending the momentum of the labor market. The RBA’s statement on monetary policy was due for release Thursday evening along with New Zealand’s 2-year inflation expectations report. Both AUD/USD and NZD/USD are trading right above key Fibonacci support and Friday’s U.S. data will determine whether these levels hold or break.

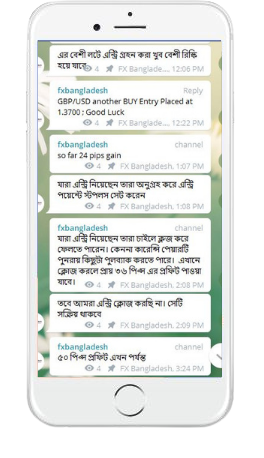

আশা করি আর্টিকেলটি আপনার ভালো লেগেছে। এই আর্টিকেল সম্পর্কিত বিশেষ কোনও প্রশ্ন থাকলে আমাদের জানাতে পারেন কিংবা নিচে কমেন্ট করতে পারেন। প্রতিদিনের আপডেট ইমেইল এর মাধ্যমে গ্রহনের জন্য, নিউজলেটার সাবস্ক্রাইব করে নিতে পারেন। গুরুত্বপূর্ণ বিষয়গুলো টিউটোরিয়াল দেখার জন্য অনুগ্রহ করে আমাদের ইউটিউব চ্যানেলটি সাবস্ক্রাইব করুন। এছাড়াও, যুক্ত হতে পারেন আমাদের ফেইসবুক এবং টেলিগ্রাম চ্যানেলে। এছারাও ট্রেড শিখার জন্য জন্য আমাদের রয়েছে বিশেষায়িত অনলাইন ট্রেনিং পোর্টাল।